If you have completed university study in the past and deferred payment then you will have an accumulated HECS-HELP debt. These can be in the order of $15,000 – $50,000. (If yours is more, I feel for you as it means you have been at university a long time)

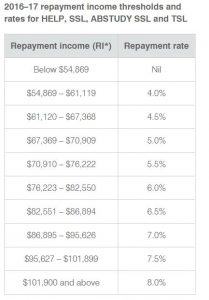

You have to start repaying your HECS-HELP debt through the taxation system once your income is above the compulsory repayment threshold of $54,869. This threshold is adjusted each year with inflation. Your employer will automatically take out the amount you are required to repay directly from your wage as long as you fill in your tax file number declaration form correctly. See the below table for these rates.

#Source ATO Website

If you are earning $65,000 per annum you will be required to repay $2,925 per annum from your wage to your debt.

Currently if you decide to pay for your studies upfront rather than utilise the HECS-HELP system you receive a 10% discount on your fees. Also if you decide you have surplus cash lying around and make a lump sum repayment of over $500 you are eligible for a 5% discount on this repayment of your fees.

These discounts mean that it is advantageous to pay upfront or as a lump sum to reduce debts faster.

There is no real interest charged on HECS‑HELP loans. However, debts will be indexed each year to reflect changes in the Consumer Price Index to maintain its real value.

The indexation adjustment is made by the Australian Taxation Office on 1 June each year and applies to the portion of debt that has been unpaid for 11 months or more.

Going back to my example, if you are completing an accounting degree for three years at the University of Tasmania this costs approximately $31,500. If you pay for this upfront you only have to dig out $28,350 (at the moment). If you decide to pay it off as a lump sum after you have started you have to dig out $29,925. The discounts provided for these payments was a definite benefit, however the government is taking this away from the 1st of January 2017.

The difference after January as to whether to pay a lump sum or just pay the regular repayments will depend on your available cashflow.

Even though this loan doesn’t have “interest” charged it is still being indexed. So if you have a lot of debts the more expensive ones would be best to pay off first but if you don’t have other debts and have available cashflow the removal of non-deductible debts is always a good plan.

If you have any questions or wish to receive advice on repayment options for your debts please let the staff at Ritchie Advice know we would be more than happy to sit down and work with you to determine exactly what options are available and how to best repay your debts.

This advice may not be suitable to you because it contains general advice which does not take into consideration any of your personal circumstances. All strategies and information provided in this article is general advice only.

Ritchie Advice Pty Ltd ABN 12 150 128 448, is a Corporate Authorised Representative 408050 of Dover Financial Advisers Pty Ltd, Australian Financial Services Licensee No. 307248.

Erin Gourlay